Dec 31, 2025

Voice-Driven Support for Microfinance: A Practical Guide for MFIs

Microfinance has become one of India’s most expansive financial ecosystems, now serving customers across 718 districts, 29 states, and 7 union territories. Its reach, especially into rural and underserved regions, has played a pivotal role in accelerating India’s digitalisation journey. Just as internet banking reshaped how consumers accessed financial services, microfinance is now entering its next major digital revolution, powered by Voice-Driven Support and AI-led automation.

As borrower volumes grow and regulatory expectations tighten, MFIs face rising pressure to deliver timely communication, improve repayment discipline, reduce operational load, and maintain consistency across multilingual regions.

Voice automation offers a transformative path forward, enabling MFIs to scale customer outreach, improve collections efficiency, and deliver compliant communication across millions of interactions. But this transformation is not without challenges. Ensuring accuracy, language adaptability, backend readiness, and regulatory alignment requires strategic planning and microfinance-specific design, not generic automation.

This blog explores the role of voice-driven support in microfinance, its most impactful use cases, the operational challenges leaders must address, and a practical roadmap for integrating Voice AI into high-volume lending operations in India.

Key Takeaways

Microfinance is entering a new AI-led voice automation era, expanding beyond manual calling to scalable, multilingual borrower communication.

Voice-driven support fixes core operational gaps like low connect rates, inconsistent messaging, high calling costs, and compliance risks.

AI voice agents automate high-volume workflows like reminders, KYC checks, PTP follow-ups, and borrower education with higher accuracy and reach.

Effective deployment requires fundamentals, including regulatory-aligned scripts, LMS integration, structured pilots, and clear performance tracking.

Cuberoot offers a microfinance-ready Voice AI platform that automates up to 70% of borrower interactions and improves efficiency across lending operations.

What Is Voice-Driven Support in Microfinance?

Voice-driven support refers to the use of automated, AI-powered voice agents to handle high-volume borrower communication across the entire microfinance lifecycle. Instead of relying solely on manual calling teams, MFIs can use intelligent voice systems that speak local languages, deliver consistent messages, and complete routine tasks at scale, even in regions with low digital literacy.

AI voice agents differ from traditional telecalling teams in several important ways. They can make thousands of simultaneous calls, follow compliant scripts every time, collect borrower responses accurately, and update systems instantly, without fatigue, delays, or variation across branches. This makes them especially effective for time-sensitive journeys like pre-due reminders, post-due follow-ups, KYC completion, eligibility checks, and onboarding confirmations.

Voice-driven support is particularly effective for rural and semi-urban borrowers because voice, not text, is the dominant communication channel. Many customers prefer natural, conversational interactions in their local languages rather than navigating SMS instructions or chat-based flows.

Voice automation meets borrowers where they are, delivering clarity, familiarity, and trust at every touchpoint, while giving microfinance institutions a scalable, reliable way to manage outreach across large and diverse borrower bases.

Core Challenges Microfinance Leaders Face Today

Microfinance institutions operate in some of the most complex customer environments, such as geographically dispersed, multilingual, low-literacy segments with high operational touchpoints.

As borrower volumes increase and expectations shift toward faster, more transparent communication, traditional calling and field workflows are becoming increasingly difficult to sustain. The result is rising operational pressure, escalating costs, and inconsistent customer engagement across regions.

Below are the core challenges microfinance leaders consistently encounter across India’s lending landscape:

Low Connect Rates for Repayment Reminders

Many borrowers are unavailable during calling hours or use basic phones with limited availability windows, leading to poor connection rates and lower on-time repayments.

Rising Cost Per Borrower Interaction

With millions of repayment reminders, follow-ups, and verification calls each month, telecalling costs continue to climb, primarily when teams must operate at full capacity year-round.

Language Barriers and Communication Inconsistency

Borrowers speak diverse regional languages and dialects. Manual calling teams often vary in language skills, resulting in inconsistent messaging and a higher risk of misunderstandings.

High Dependency on Large Telecalling Teams

Most MFIs rely on large, centralized calling teams or outsourced partners. Scaling up or down quickly is expensive and operationally challenging, especially during peak cycles.

Operational Pressure During Disbursement Peaks

Disbursement seasons create massive spikes in verification calls, onboarding follow-ups, and repayment education, pushing support teams to the limit.

Difficulty Tracking 100% of Call Attempts and Customer Responses

Manual logs, partial reporting, and inconsistent data capture make it difficult to maintain reliable borrower communication trails or measure operational effectiveness.

Compliance Risks in Manual Calling Processes

MFIs must follow strict communication guidelines. Manual processes often lead to deviations from approved scripts, missed disclosures, or non-uniform borrower treatment, all of which increase compliance exposure.

How Voice-Driven Support Solves These Microfinance Challenges

Voice-driven automation directly addresses the operational bottlenecks that microfinance institutions face as they scale. By combining multilingual calling capability, standardized communication, and real-time system updates, AI-powered voice agents remove the friction that slows down borrower outreach and collections. Here’s how voice automation strengthens everyday MFI operations:

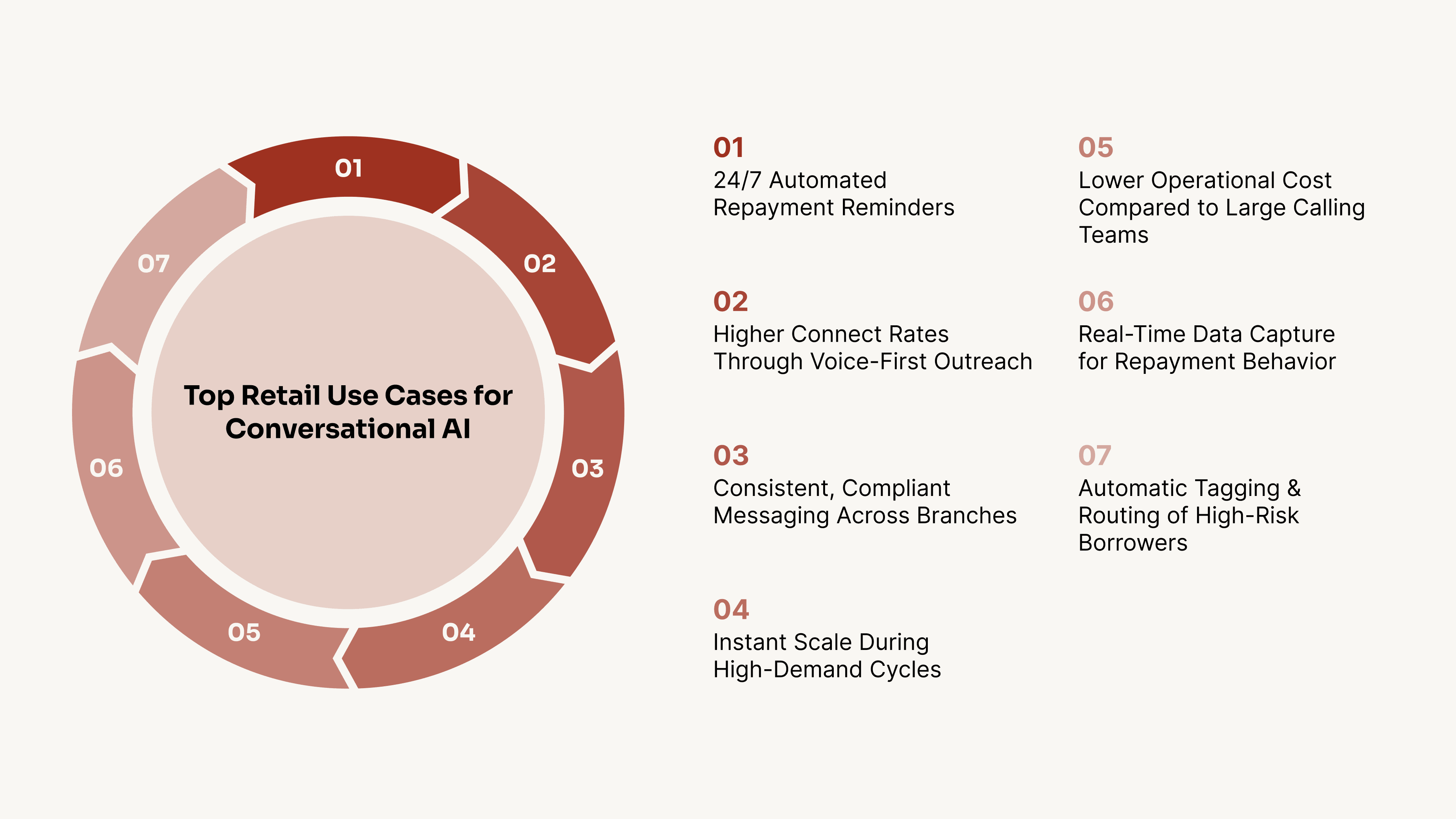

24/7 Automated Repayment Reminders

Voice agents can reach borrowers at any time of day—even outside standard calling hours, ensuring reminders are delivered when borrowers are more likely to answer. This improves visibility into EMI dates and reduces delays caused by missed communication windows.

Higher Connect Rates Through Voice-First Outreach

Rural and semi-urban borrowers prefer voice over text. Automated voice calls achieve significantly higher pickup and engagement rates, especially for reminders, KYC prompts, and delinquency follow-ups, where timing and clarity are crucial.

Consistent, Compliant Messaging Across All Branches

Voice-driven systems deliver the same approved script, tone, and disclosures for every borrower, regardless of region or branch. This eliminates variations caused by manual calling and reduces compliance risk across thousands of daily interactions.

Instant Scale During High-Demand Cycles

During disbursement seasons or delinquency spikes, voice automation can handle thousands of calls simultaneously—something even large telecalling teams cannot match. MFIs avoid emergency hiring and still maintain timely communication across all borrower segments.

Lower Operational Cost Compared to Large Calling Teams

Automating routine reminders, follow-ups, and verification calls reduces the need for costly outbound calling. MFIs can redirect human agents to more complex or sensitive cases, while the AI handles repetitive, high-volume tasks.

Real-Time Data Capture for Repayment Behavior

Voice agents log responses instantly, such as intent to pay, preferred dates, customer queries, or reasons for delay. This gives collections and risk teams actionable borrower insights and improves prioritization of follow-up workflows.

Automatic Tagging and Routing of High-Risk Borrowers

If a borrower indicates distress, confusion, or inability to pay, the system can automatically flag the account and forward it to the right collections or field officer. This early visibility is critical for preventing NPAs and stabilizing delinquency buckets.

6 High-Impact Use Cases for Voice-Driven Support in Microfinance

Voice-driven support is being executed globally, and with AI, new use cases are emerging that go far beyond traditional calling workflows. These capabilities are especially valuable for microfinance, where scale, multilingual access, and compliance are critical. Here are practical use cases your MFI can start implementing right away.

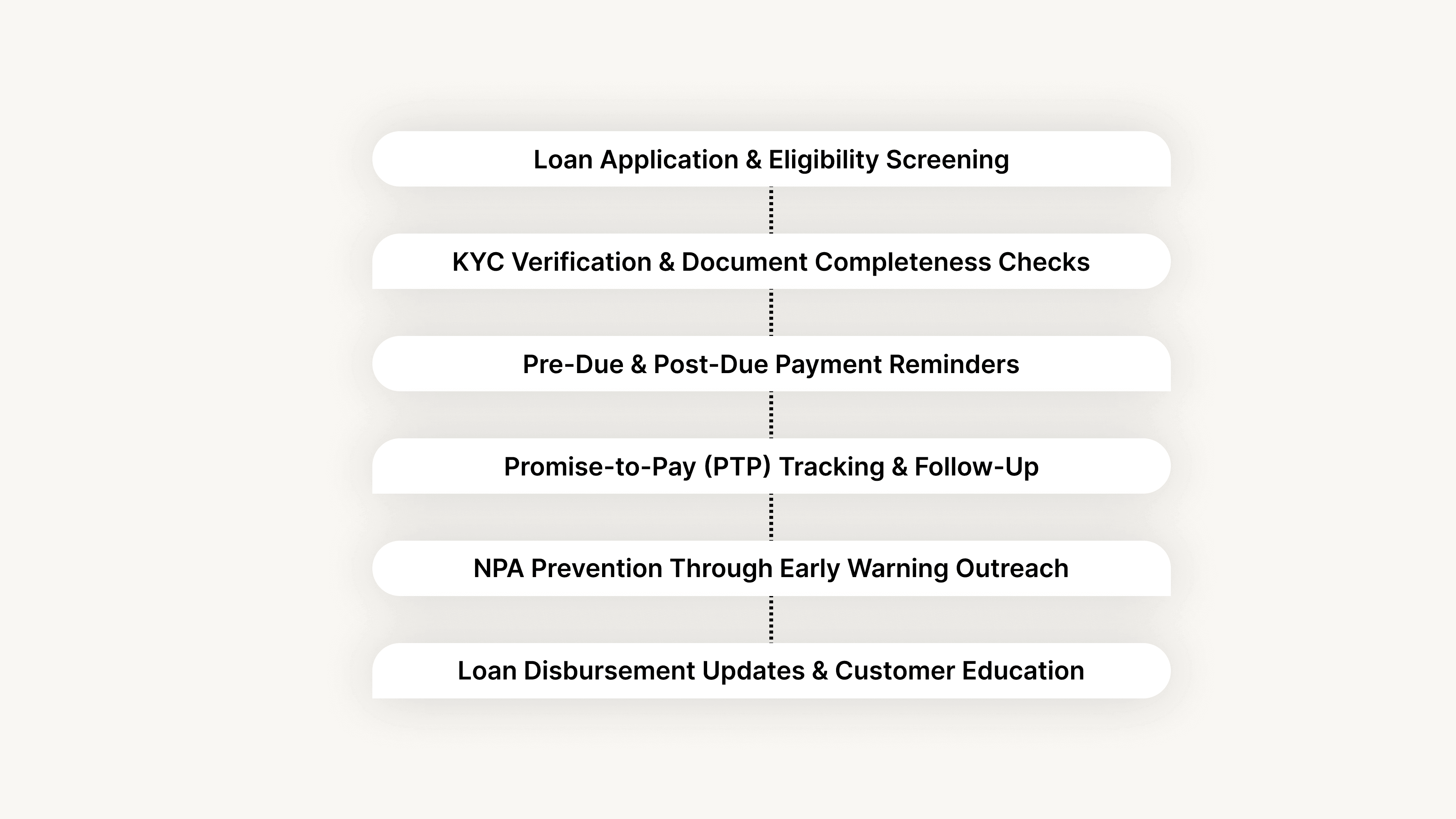

1. Loan Application & Eligibility Screening

Voice-driven screening verifies customer details before a field officer visits the borrower, reducing wasted trips and improving lead quality. It ensures only genuinely interested and eligible applicants move to the next stage.

Example: An automated voice call confirms income range, loan purpose, and availability for verification, filtering out low-quality leads before assigning them to field staff.

2. KYC Verification & Document Completeness Checks

Automated follow-up calls remind borrowers to submit pending documents and confirm what’s missing, enabling faster onboarding and compliance adherence.

Example: The system calls borrowers to inform them that their Aadhaar copy is pending and guides them to the nearest branch or upload option.

3. Pre-Due & Post-Due Payment Reminders

Voice AI delivers clear repayment reminders in borrowers’ preferred languages, ensuring they are aware of due dates and overdue amounts. These reminders drive higher on-time repayments with minimal manual effort.

Example: A day before EMI, borrowers receive a reminder call explaining the exact amount, date, and available repayment channels.

4. Promise-to-Pay (PTP) Tracking & Follow-Up

Voice agents automatically follow up based on the borrower’s previous commitment, ensuring timely action and reducing the load on collections teams.

Example: If a borrower promised to pay on Friday, the system triggers a confirmation call on Thursday to validate intent and adjust follow-up plans.

5. NPA Prevention Through Early Warning Outreach

MFIs can reach borrowers showing early signs of distress like missed attempts, partial payments, or repeated deferrals, before they slip into higher delinquency buckets.

Example: Borrowers with two missed reminders receive an early-warning call asking if they need assistance or a revised schedule, enabling proactive intervention.

6. Loan Disbursement Updates & Customer Education

Automated voice calls guide borrowers through disbursement details, EMI schedules, repayment modes, and branch support information, reducing confusion and increasing financial literacy.

Example: After loan approval, borrowers receive a call explaining when funds will reflect, how EMIs will be calculated, and whom to contact for issues.

Also read: Conversational AI for Finance: Transforming Financial Services

How to Implement Voice-Driven Support in an MFI (Step-by-Step Guide)

Businesses often implement voice-driven support like AI agents without first addressing the fundamentals, leading to poor borrower experience, low accuracy, and operational failures.

Successful implementation requires aligning technology with borrower behavior, regulatory rules, and existing systems. Here is a practical, structured approach MFIs can use to deploy voice-driven support the right way.

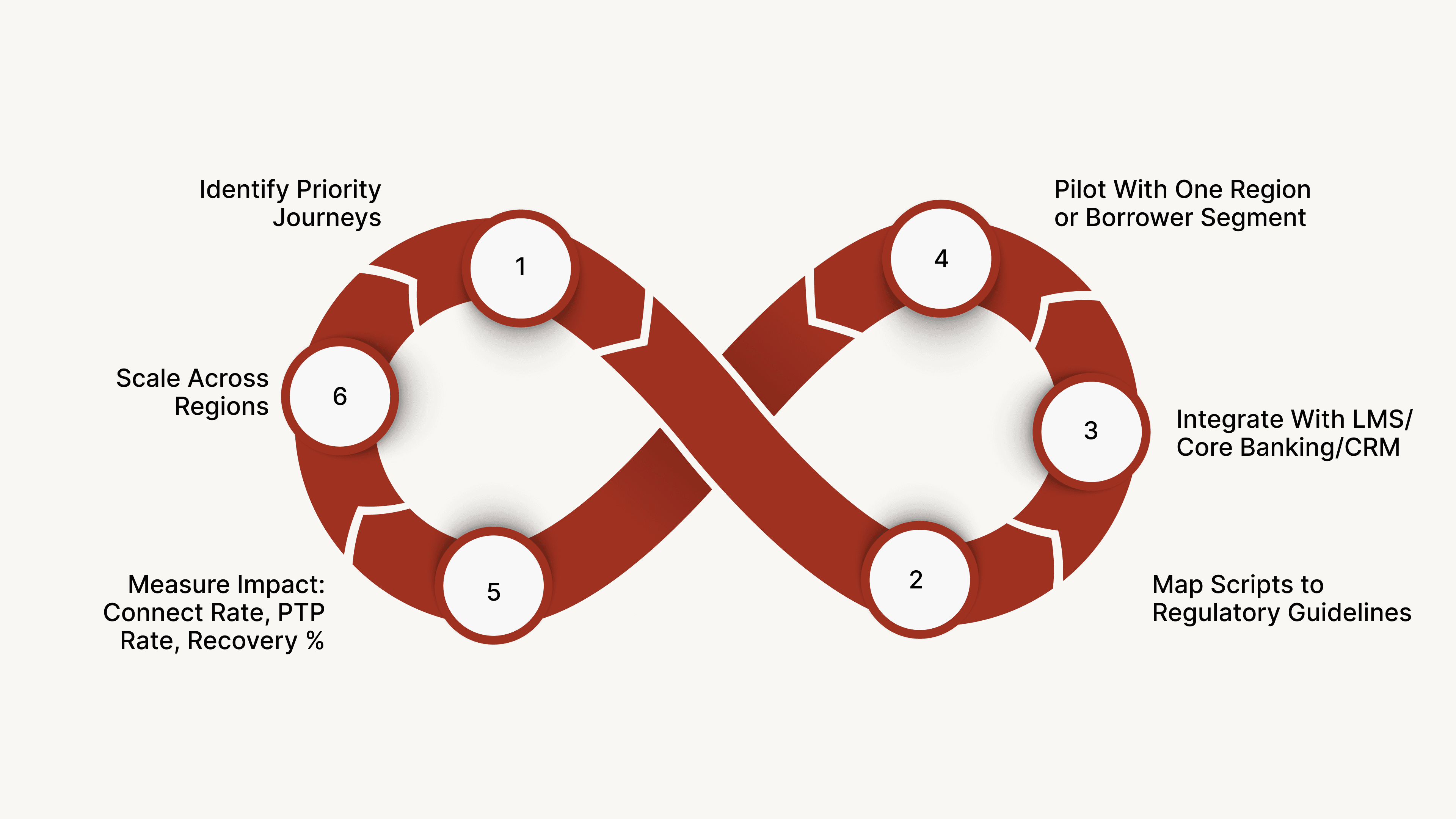

Step 1: Identify Priority Journeys (Pre-due, post-due, onboarding, KYC)

Before deploying Voice AI, MFIs must identify the borrower interactions that create the highest workload or have the biggest repayment impact. These journeys should be automated first to ensure quick wins and measurable improvements.

Key focus areas:

Pre-due reminders.

Post-due follow-ups.

KYC and document-verification calls.

Onboarding welcome calls.

Eligibility and field-visit confirmation.

Early-warning outreach for at-risk borrowers.

Step 2: Map Scripts to Regulatory Guidelines

Microfinance communication is highly regulated, especially around repayment behavior, disclosures, tone, and borrower treatment. Ensuring scripts follow guidelines from RBI and SROs (MFIN/Sa-Dhan) is essential for compliance and consistency.

What to validate:

Mandatory disclosures and tone requirements.

Clear, respectful communication wording.

No coercive or high-pressure language.

Script variations for reminders vs. delinquency calls.

Regional language versions reviewed for accuracy.

Step 3: Integrate With LMS/Core Banking/CRM

Voice automation becomes powerful only when it is connected to live borrower data. Integration ensures that reminders, follow-ups, and verifications are based on accurate loan information.

Integration essentials:

Loan Management System (LMS) for EMI schedules and DPD status.

Core banking system for disbursement and repayment updates.

CRM for customer history and ticket tracking.

APIs for recording call outcomes and borrower responses.

Step 4: Pilot With One Region or Borrower Segment

A targeted pilot reduces risk and helps teams validate messaging, connect rates, and workflow accuracy before scaling. MFIs should choose one territory, product line, or borrower group for the initial rollout.

Pilot guidelines:

Start with one language or region.

Select a specific journey (e.g., pre-due reminders).

Track connect rate, borrower feedback, and operational improvements.

Gather field and branch feedback for refinements.

Step 5: Measure Impact: Connect Rate, PTP Rate, Recovery %

Once the pilot is active, MFIs should continuously track performance to understand where automation is working well and where refinements are needed.

Metrics to monitor:

Connect rate (outbound calls answered).

Promise-to-pay rate (commitment captured).

On-time repayment improvement.

Borrower sentiment across calls.

Reduction in manual calling workload.

Movement in delinquency buckets (DPD 1–30, 30–60, etc.).

Step 6: Scale Across Regions & Product Lines (JLG, Individual Lending, MSME)

After validating results, MFIs can expand automation across languages, regions, and lending products. Scaling ensures consistent, compliant communication across the entire borrower base.

Scaling priorities:

Add regional languages (Hindi, Tamil, Telugu, Bengali, Kannada, etc.)

Expand automation to multiple journeys, including KYC, onboarding, and early-warning.

Enable Voice AI for JLG, individual lending, and MSME borrowers.

Standardize reporting across branches for better operational control.

Related: Top AI Voice Assistants in 2025

Why Cuberoot Is Built for Microfinance Voice Automation

Microfinance teams need automation that is fast, multilingual, compliant, and able to manage massive borrower volumes without stressing calling teams. Cuberoot delivers exactly that: an AI-driven voice platform tailored to Indian lending workflows, including collections, verification, onboarding, reminders, and follow-ups.

CubeRoot's voice-first approach helps MFIs reduce operational pressure, improve repayment behavior, and maintain consistent borrower communication across regions.

Key Features & Advantages:

Boost operational efficiency by up to 60% with automated borrower communication across pre-due, post-due, and verification cycles.

Reduce wait times by 90% with instant, multilingual voice interactions that avoid agent bottlenecks.

Ready Voice AI agents for collections, lead qualification, payment follow-ups, and borrower support (Hindi + English, human-like voices).

40% improvement in CSAT due to natural, lifelike conversations that borrowers understand and trust.

Automate 90% of inbound and outbound enquiries through 24/7 self-service flows.

50+ prebuilt integrations with LMS, CRMs, core banking systems, and payment solutions for rapid deployment.

Launch within 14 days using industry-ready templates for repayment reminders, PTP tracking, onboarding calls, and early-warning outreach.

Unlimited concurrent calls at a fraction of the cost—ideal for peak collection cycles or large repayment batches.

Multilingual coverage across India with no additional licensing or per-language costs.

Enterprise-grade compliance with automated QA, audit logs, script adherence, and data privacy controls.

Cuberoot enables MFIs to deliver accurate borrower communication at scale, reducing manual calling load, improving repayment discipline, and bringing consistency across all branches and field teams.

Ready to transform your borrower communication and collections workflows? Book a Cuberoot demo today and see how Voice AI can automate up to 70% of your microfinance operations, accurately, securely, and at scale.

Conclusion

Microfinance has played a defining role in India’s digitalization journey, bringing financial access to millions across underserved and unbanked communities. As the sector expands across districts, states, and borrower segments, it now stands on the brink of another major transformation, one that strengthens both customer experience and operational efficiency. Voice-driven support powered by AI voice agents is the next revolution, enabling MFIs to communicate clearly, consistently, and compliantly at massive scale.

Adopting Voice AI doesn’t just help automate calls; it helps borrowers understand their obligations better, improves repayment discipline, reduces friction for field teams, and gives MFIs a way to manage high volumes without increasing costs. It benefits people and institutions alike, creating a more transparent, responsive, and resilient lending ecosystem.

And for MFIs that need a specialized platform built for the realities of Indian microfinance, Cuberoot offers a voice-first, multilingual, compliance-ready solution designed to handle collections, onboarding, reminders, PTP tracking, and borrower education, securely and at scale.

Ready to modernize your microfinance operations with Voice AI? Schedule a Cuberoot demo today and see how automated, multilingual voice agents can transform your borrower communication at scale.

FAQs

1. Can Voice AI adapt to varying borrower profiles, such as JLG groups and individual lending customers?

Yes. Voice AI can be configured with different scripts, languages, and workflows for Joint Liability Groups, individual borrowers, MSME clients, or region-specific segments. Each borrower type can receive customized communication aligned to their repayment pattern and product structure.

2. How does Voice AI handle borrowers who use feature phones or have limited network connectivity?

Voice-driven support works seamlessly with basic phones since it relies on simple inbound/outbound calling. Even in low-connectivity regions, call retries, timing optimization, and scheduled outreach ensure higher pickup rates compared to SMS or digital app notifications.

3. Can Voice AI support field officers, or is it only for borrower communication?

Voice AI can assist field staff by sending visit reminders, updating them on escalation cases, and sharing last-minute changes in borrower commitments. It becomes a support layer for both customers and operational teams.

4. What happens if a borrower provides incorrect or conflicting information during an automated call?

Voice AI can request clarification, route the call to a human agent, or flag the borrower for a follow-up by the collections or verification team. This prevents incorrect data from entering the system and ensures proper handling of exceptions.

5. Can MFIs customize call frequency and timing to match their internal collection strategies?

Absolutely. Call schedules can be configured based on DPD bucket, borrower behavior, preferred language, repayment cycle, and regional norms. MFIs can define timing windows to ensure communication remains borrower-friendly and compliant.